”[...] there is reason to worry that in the coming weeks the situation in agriculture – both within Ukraine and, as a result, globally – could take a turn for the worse.

Prof. Dr. Stephan von Cramon-TaubadelDepartment of Agricultural Economics and Rural Development

Background

Seven months after Russia’s attempted invasion of Ukraine began, we know much more about its effects on agriculture in Ukraine, on international agri-food markets, and on global food security. These topics have been the focus of many insightful analyses [2] and countless conferences, workshops, interviews and articles in print and online media.

The invasion as such has failed, but Russia initially occupied roughly 20% of Ukrainian territory and has rained death and destruction on large parts of the rest. In recent weeks Ukrainian forces have liberated substantial amounts of occupied territory. In response, the Russian dictator has introduced conscription to shore up his flagging military, staged sham referenda as a pretence for the annexation of parts of Ukraine, and made thinly-veiled threats that, if pushed, he would use nuclear weapons to achieve his ends. These moves are widely interpreted as acts of desperation by a dictator whose agenda is spinning out of control.

Against this background there is reason to worry that in the coming weeks the situation in agriculture – both within Ukraine and, as a result, globally – could take a turn for the worse. Over the last two months, Ukraine has exported grains and oilseeds at a surprising clip. The Black Sea corridor that was negotiated with the assistance of Turkey and the United Nations in late July has performed well, even exceeding expectations. However, this corridor does not have sufficient capacity to handle Ukraine’s entire export potential. Furthermore, the Black Sea corridor operates at the whim of a Russian dictator who could shut it down at amoment’s notice, and has already hinted at his inclination to do so.

This highlights the importance of the land route via Ukraine’s southern and western EU neighbours as a complement to, and if necessary, a substitute for exports via the Black Sea corridor. Unfortunately, the land route has not performed up to expectations in recent months. This is having a devastating effect on Ukrainian agriculture. In addition, it is increasing the dependence of Ukrainian agriculture and global food security on a grain ‘pipeline’ through the Black Sea that is every bit as vulnerable as the sabotaged Baltic Sea gas pipelines that have been headline news in recent days. In the following I describe the current state of grain and oilseed markets and exports in Ukraine, and discuss some old and new problems that could and should be resolved.

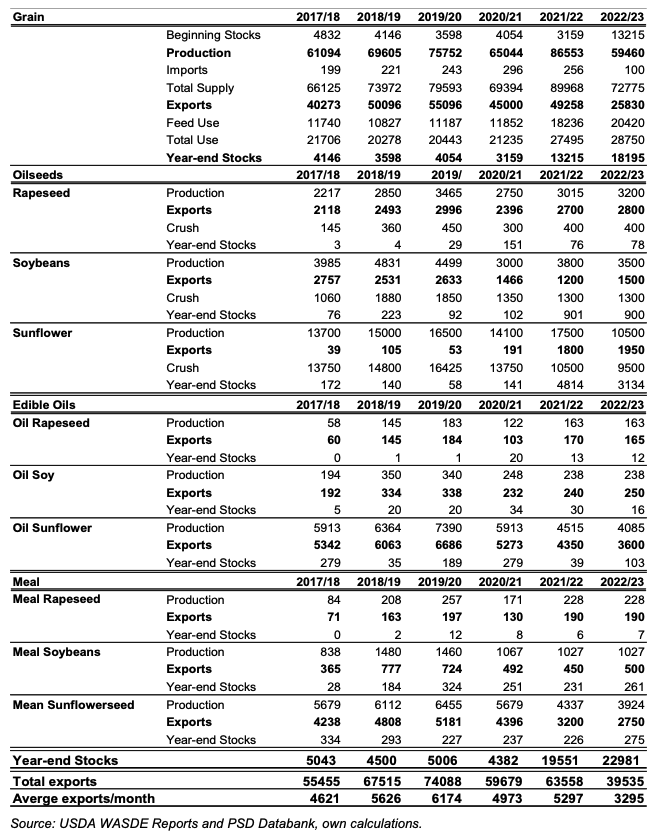

1. This year’s production and export surpluses in Ukraine

Barley, rapeseed, rye and wheat harvests in Ukraine have been completed, at least in those places where it was possible to harvest. The maize, sunflower seed and soybean harvests have begun and will continue into November. The USDA’s most recent WASDE Report (September) estimates 2022 grain production in Ukraine at roughly 59.5 mt, including 20.5 mt of wheat, and 6.4 mt of barley. As weather conditions in the region have been favourable, the USDA has increased its estimates of maize production from 25 mt in the July WASDE report to 31.5 mt in the September report. The USDA predicts that sunflower seed, soybean and rapeseed production will reach 10.5, 3.5 and 3.2 mt, respectively, putting total oilseed production at 17.2 mt (see Table 1).

Altogether, the USDA thus predicts that this year’s total crop production in Ukraine will add up to approximately 76.7. This is more than the 67 mt that the Ukrainian Ministry of Agriculture has forecast [3]. The USDA’s considerably more optimistic estimates of maize production explain much of the difference.

The big challenge the next months will be getting this production to market. This is important not only for the countries that depend on imports and for global food security, but also for farms in Ukraine, which desperately need liquidity from the sale of this year’s crop to pay wages and, crucially, to finance the seeding of next year’s crop.

How much of the production estimated above is available for export? In its WASDE reports, the USDA estimates not only production but also domestic use, trade and closing stocks for each marketing year. In its September report, it estimates that Ukraine will export 25.8 mt of grain in 2022/23, as well as 6.3 mt of oilseeds, 4.0 mt of vegetable oil, and 3.4 mt of oil meal (Table 1). Altogether, the USDA is predicting that Ukraine will export roughly 39.5 mt of grains, oilseeds and oilseed products in the 12 months from July 2022 through June 2023. However, Ukraine’s export potential over this period is much greater than 39.5 mt.

Table 1: Ukraine grain and oilseeds supply and demand (‘000 t)

In its estimates, the USDA assumes that domestic use of grain in Ukraine will increase from an average of roughly 21 mt in the marketing years between 2017/18 and 2020/21 to well over 27 mt in 2021/22 and 2022/23. This assumption is puzzling, and it has been questioned by many observers. Given the substantial numbers of refugees who have left Ukraine, and the expected reduction in animal numbers and therefore feed demand in the country, if anything one would expect domestic use of grain to fall rather than increase. Furthermore, the USDA also predicts that year-end stocks of grain in Ukraine will increase. In past years, year-end stocks have amounted to between 3 and 4 mt, which is equivalent to roughly 20% of annual domestic use. However, according to the USDA estimates, stocks grew to 13.2 mt by the end of June 2022, and will grow further to 18.2 mt by the end of June 2023, which is equivalent to roughly 65% of annual domestic use.

Based on these numbers, a realistic estimate of Ukraine’s grain and oilseed export potential lies somewhere between 55 and 60 mt. These include the 39.5 mt of exports that the USDA is predicting, plus at least 7 mt that result from correcting the USDA’s inflated domestic use estimates, plus perhaps 13 mt out of estimated year-end stocks.

2. Getting grains and oilseeds to market – logistical bottlenecks

Regardless of how much is ultimately exported – 39.5 mt or a larger amount – the logistical challenge is huge. Even exporting ‘only’ 39.5 mt in the 2022/23 marketing year would require average monthly exports of almost 3.3 mt; exporting 55 to 60 mt would require average monthly exports of 4.5 to 5 mt.

• By sea

Since the opening of the Black Sea corridor, grain and oilseed exports can leave Ukraine by sea via the ports in Odessa, Chornomorsk and Pivdennyi (sometimes referred to as the ‘Odessa port range’). On September 27, eight weeks after the corridor was opened, the Istanbul-based Joint Coordination Centre (JCC) responsible for its operation announced that 5.3 mt of agricultural goods had been exported via this route, for a weekly average of 0.65 mt [4]. JCC data suggest that 1.2 mt left the Odessa port range in the third week of September alone.

This is most impressive. Ukraine has exported as much as 6 mt per month in past years (see Table 1), but many of the ports that contributed to this throughput – such as Mykolaiv, Kherson, Mariupol and Berdyansk – are heavily damaged and occupied by Russia. One month ago, experts were claiming that the Odessa port range could handle no more than 2 mt per month. However, the most recent export volumes reported by the JCC indicate that over 4 mt per month are possible.

This suggests that port operators and traders are responding to powerful incentives. It is reported that while the current price of corn fob Ukrainian Black Sea port is roughly 260 €/t, the price of corn delivered to Black Sea ports in Ukraine is 220 €/t. A fobbing margin of 40 €/t certainly is a powerful incentive for port operators to maximise throughput; over the exports of 5.3 mt recorded by the JCC it adds up to over 200 million Euros.

Could Ukrainian farmers farther inland be getting more for their grain? No question. In an export situation the farmer receives a farm-gate price that equals the fob price at the nearest port, minus fobbing costs and the cost of transporting the grain from the farm to that port. 220 €/t delivered to a Black Sea port, minus transport cost from central Ukraine of roughly 50 €/t, leaves the farmer with a farm-gate price of perhaps 170 €/t. If the fobbing costs could be reduced, this farm-gate price would increase correspondingly. I return to this issue below. For the moment, however, the good news is that Ukraine is exporting grain and oilseeds at a faster pace than many had anticipated.

Can this pace be maintained? Presumably yes, if the Black Sea corridor remains open, and the ports themselves and the inland infrastructure that supports them, such as rail lines and grain silos, are not (further) damaged by Russian rockets. Both of these assumptions are questionable. On September 6, Russian Foreign Minister Lavrov criticised the operation of the Black Sea corridor. President Putin followed up with similar remarks on September 7, claiming that Russia was being cheated by the implantation of the corridor, maintaining that most of the exported grain was being shipped to Europe and not to low-income importing countries that were facing famine, and complaining about a lack of reciprocity for Russian exports [5].

Hence, when the agreement to open the corridor expires after 120 days at the end of October, it is far from certain that Russia will agree to an extension. In addition, even while it remains formally open, the corridor is always just one rocket attack away from effective closure. In recent weeks, as Ukrainian armed forces have achieved significant victories over Russian invaders in Eastern Ukraine, Russia has renewed its threats to attack Ukrainian infrastructure. On September 25, Ukrainian military authorities claimed to have shot down several Iranian made drones over the water close to the ports of Pivdennyi and Odessa [6].

The USDA estimates that Russia will harvest a bumper wheat crop of 91 mt this year, up from 75 mt in 2021. Some analysts are predicting that the Russian harvest might even reach 100 mt. With its own export surpluses piling up and global shipping capacity in short supply,

Russia has little interest in a Black Sea corridor that both helps Ukraine and increases the competition that Russian exports face on global markets. In addition, closing the corridor would be yet another provocation that the Russian dictator could use to pressure and attempt to sow discord among the countries that oppose him. The Black Sea corridor is an encouraging accomplishment that holds much hope for global food security and for farmers in Ukraine, but it hangs by a thread.

• By land

Even if the Black Sea corridor continues to function, it will be hard-pressed to handle the 4.5 to 5 mt of potential monthly exports outlined above. Furthermore, the farm-gate price calculations presented above hold for locations in central and southern Ukraine. Farms in western regions of the country are farther away and the prices that they can receive for shipping to the Odessa port range are correspondingly lower. For these farms, the land route via Romania, Hungary, Slovakia and Poland is the preferred option.

Given the importance of the land route, it is frustrating that it continues to underperform. Before agreement on the Black Sea corridor was reached, the need to facilitate grain and oilseed exports via the land route received a great deal of attention in the media and in policy circles in both Ukraine and the EU. High-level meetings took place and pledges were made. On May 12, the EU Commission proudly announced the establishment of ‘Solidarity Lanes’ to facilitate Ukrainian exports of agricultural goods. EU Transport Commissioner AdinaVălean stated: “20 million tonnes of grains have to leave Ukraine in less than three months using the EU infrastructure. This is a gigantesque challenge, so it is essential to coordinate and optimise the logistic chains, put in place new routes, and avoid, as much as possible, the bottlenecks.” [7]

Unfortunately, when all is said and done, more has been said than done. Trucks still spend many days in line-ups at border crossings. Delays of 5 days and more leaving Ukraine are the rule, and re-entering often involves an additional wait of several days. On August 18 one Ukrainian farmer called in from kilometre 38 of such a line-up at a western border crossing; two days later he had ‘advanced’ to kilometre 20. On September 17 a Ukrainian trucker reported that he had been waiting 12 days at the Polish border with a cargo of corn destined for the Netherlands [8]. Chats and social networks are full of similar complaints by exasperated traders, Ukrainian farmers, and EU farmers who have invested in or manage farms in Ukraine. Recent reports in late September point to some improvement, but the land route nevertheless continues to underperform.

The economic costs of excessive delays at border crossings are immense. First, delays tie up transport capacities and reduce export volumes. A truck can cover roughly 600 km in one day, and the 1200 km distance from L’viv to Rostock is typical of the distances that truckloads of Ukrainian export grain must travel. Hence, a return trip should take no more than four days, or five days if we add one day for loading and unloading. A truck with a payload of 22 t should therefore be able to make six trips per month, and move a total of 132 t in the process. A seven-day delay inflates the total turn-around time from five to 12 days: instead of six trips only 2.5 are possible, and the monthly volume of shipment per truck is more than halved to 55 t.

Second, border delays increase the transport costs per ton of exports. In Germany a truck typically costs between 650 and 700 €/day including the driver’ wage, fuel and deprecation. In Ukraine the costs are lower, perhaps 500 €/day. Since a truck that is waiting in line uses less fuel, actual costs might be lower, say 300 €/day. Under these assumptions, seven days of waiting at the border cost €2100, or roughly €95 for each of the 22 t of payload. Those 95 €/t are effectively a tax on the farm-gate price received by Ukrainian farmers. If the current price fob Gdansk is 330 €/t and typical transport costs from Ukraine to Gdansk, without unnecessary delays, amount to 130 €/t, then the farmer can expect to receive a farm gate price of 200 €/t. If unnecessary delays increase the transport costs by 95 €/t to 225 €/t, then the farm gate price will fall to 105 €/t.

This also has implication for the pricing and margins of exports via the Black Sea corridor that were mentioned above. The best corrective for large margins is competition. Currently, traders and Odessa port range operators do not have to compete for grain. The less pull the land route exerts, the farther the geographical boundary between those regions that export via the Black sea and those that export via the land route shifts to the north and west. The larger their catchment area, the more market power that traders and port operators can exercise over grain and oilseed supplies in central and southern Ukraine.

Delays at the border are therefore substantially reducing the prices that farmers in Ukraine are receiving for their grains and oilseeds. This destroys value and deprives farmers of revenue that they desperately need to pay their employees and put a crop in the ground for next year. A reduction in farm gate prices of 95 €/t multiplied by the 2022 grain and oilseed harvest of 73 mt implies a total loss in revenue for Ukrainian agriculture of almost €7 billion. These are, admittedly, rough calculations. But even one half of that amount would represent a major loss to farmers and the agricultural sector in Ukraine.

3. What can be done?

What is causing delays at the border, and why have they persisted despite all of the promises and pledges? It is understandable that delays took place back in April and May; Ukraine had never exported large quantities of grains and oilseeds westwards by land, suitable infrastructure was not in place, and customs and inspection officials were unprepared. In the meantime, however, there has been plenty of time to commit resources and streamline procedures.

It appears that two factors are contributing to the current situation. First, anecdotal evidence suggests that corruption in the Ukrainian customs administraton is playing a role; delays can be shortened and border formalities accelerated, for a price. Corruption affects customs administrations in many countries, and for years Ukraine has ranked among the most corrupt countries in Europe [9]. Ukraine cannot afford this sort of institutional rot, now less than ever. Since Russia’s aggression began, Ukrainian leaders have rightly praised the country’sfarmers for their heroic efforts under often life-threatening conditions. Corruption that takes money out of farmers’ pockets makes mockery of that praise. Furthermore, corruption needs to be confronted and reduced as a part of Ukraine’s preparations for EU accession. A possible first step would be to plant law-enforcement officials on trucks crossing the border and make some public arrests of any officials who request or accept bribes.

Second, there are indications that most of the current delays are due to customs and inspections procedures on the EU side of the border. Farmers in a number of neighbouring EU member states – such as Bulgaria and Romania – are complaining that low-priced grain from Ukraine is depressing prices on their local markets. Complaints by farmers in Eastern Poland appear to be having the largest effect. Ukrainian grain on the way to Baltic ports such as Gdansk and Rostock passes through Polish border crossings, and reports suggest that grain prices in eastern Poland are as much as 40 €/t lower than in western parts of the country. Polish officials deny that they are deliberately hindering the flow of grain in response to pressure from domestic farmers. However, many reports confirm that understaffing and exaggerated procedures are substantially impeding cross-border movements.

Ukrainian authorities are hesitant to criticise Poland, which has so staunchly supported Ukraine before and throughout the current crisis. The EU can and should remedy the situation in collaboration with Polish authorities. Staffing at border crossings should be increased, and better coordination between customs officials across member states would help ensure that more grain that enters from Ukraine transits through the EU on its way to international markets and is not unloaded shortly behind the border within the EU. If delays at the border were reduced, truckers would feel less pressure to unload quickly in an attempt to make up for lost time – hence they would be more likely to transit through to destinations farther north and west in the EU. In addition, a temporary support package for farmers in regions that border on Ukraine could help to relieve the political pressure that is at the root of the problem [10].

4. Outlook

Time is very short. Ukrainian farmers are making decisions today about how much and what to plant in the coming months. The Ukrainian Ministry of Agrarian Policy expects that as much as 35% less grain will be seeded than last year [11]. Many farmers who currently lack the financial means to purchase inputs are sowing fewer winter crops (especially wheat) and hoping that they will be able to compensate by sowing more summer crops (such as corn and sunflower) next spring. Moreover, farmers are focusing the scant liquidity that they have on planting oilseeds such as rapeseed rather than wheat, because oilseeds are more profitable. The shift to oilseeds can be expected to continue next spring, with Ukrainian farmers planting more soybeans and sunflower at the expense of wheat, corn and barley. Delays at the border and inflated transport costs and margins are fuelling this switch; when transport capacities are limited, it makes sense to dedicate them to goods such as oilseeds (and their by-products oil and meal) that have the highest value per ton.

Reduced crop production in Ukraine coupled with the shift from grains to oilseeds threatens to prolong the reduction in Ukraine’s contribution to world markets and global food security to the 2023/24 marketing year and possibly beyond. Markets are anticipating this effect; wheat futures prices for the 2023 crop (e.g. September and December 2023 MATIF wheat contracts) have been creeping steadily upwards, from under 280 €/t in late July to currently just under 330 €/t [12]. While the Black Sea corridor has provided valuable short-term relief, the situation is extremely fragile. The land route must urgently be optimised and expanded to complement the corridor and, in all likelihood, completely replace it.

References

[2] See for example:

- Glauben et al. (2022), The war in Ukraine exposes supply tensions on global agricultural markets: Openness to global trade is needed to cope with the crisis. IAMO Policy Brief No. 44, https://www.iamo.de/fileadmin/user_upload/Bilder_und_Dokumente/05- publikationen/IAMO_Policy_Brief/IAMO_Policy_Brief_44_ENG.pdf

- Abay et al. (2022), The Russia-Ukraine crisis: Implications for global and regional food security and potential policy responses. IFPRI MENA Working Paper 39, https://doi.org/10.2499/p15738coll2.135913

- FAO (2022), Ukraine humanitarian response update, https://www.fao.org/3/cc2004en/cc2004en.pdf

[6] https://www.reuters.com/world/europe/russia-steps-up-attacks-with-iranian-drones-ukraine-plans-defences- officials-2022-09-26/

[8] See https://www.wsj.com/articles/ukraine-grain-flowing-into-eu-tests-european-solidarity-11663419604

[11] See https://www.dw.com/en/ukraine-war-how-the-russian-invasion-is-changing-farmers-crops/a-63073936 and https://www.agriculture.com/news/business/high-input-prices-imperil-2023-crops-in-ukraine

[12] As of September 30. See https://www.kaack-terminhandel.de/euronext/weizen